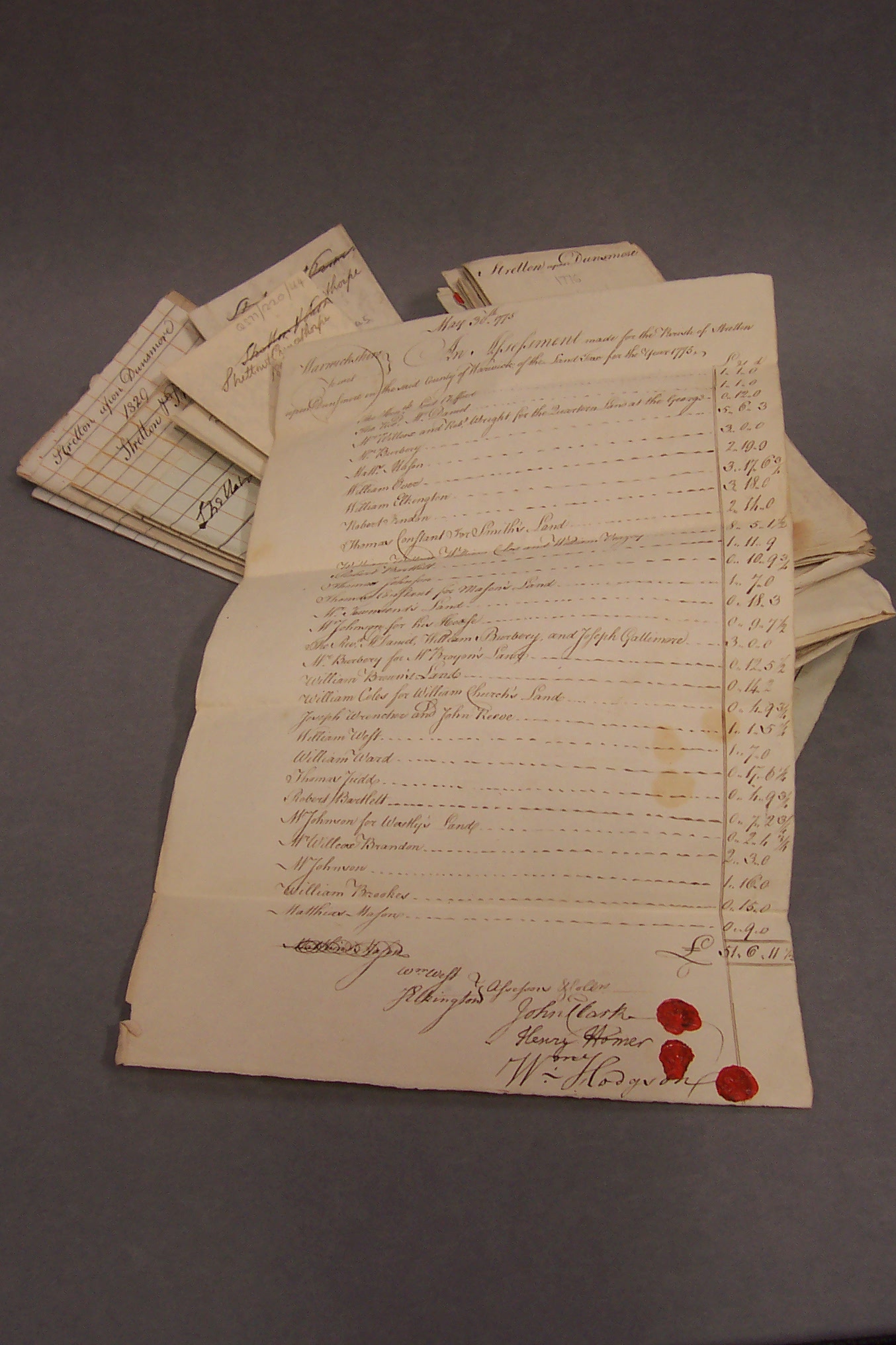

Land Tax was one of the innovative schemes of the British government to increase revenue. Introduced in 1692, in the reign of William III and Mary, and finally abolished in 1963, it was administered at the local level, and based on a tax quota for each parish which did not change from year to year.

Land tax assessment records are useful to historians because they list year by year the names of the owners of property in each parish and the sum assessed, and (in theory at least) the names of the occupiers. They also give some indication of their social standing [Titles such as Reverend, Dr., Sir, Esquire and Mr.(a gentleman) are used to define status]. Early assessments sometimes contain the minimum of information. From 1798, common printed forms were introduced, though they were not universally used until later. Some parishes still drew up their own hand-written version of the form. The later returns also give a brief description of the property.

Not named individually

Not everyone was named individually – e.g. the occupiers of a row of tenements may be listed as “John Smith and others”, and tenants of small pieces of land may not be listed individually. Where families shared a dwelling or piece of land, only the main occupier was listed. First names are not always recorded – names such as “Evans and others” or “Widow Green” may be used. The word “ditto” can be confusing. Male heads of household are always listed, where they exist, and other members of the household will not be mentioned. The link between one occupier and the next is not often stipulated, so it may be hard to work out the family relationship, if any, without referring to parish registers or other records.

The sums assessed did not change year to year, so where a sequence of Land Tax Returns survives, it is possible to trace the title to a property from 1780-1832. Names or descriptions of estates or property are not always detailed, though the names of individual large properties like farms, mills and inns are usually given. Sometimes the term “house and garden” is the only description used and the property has to be identified from others of the same description by the amount of tax assessed on it, [or by an initial reference to title deeds or leases]. The position of the property in the list when compared to other properties is usually also consistent from year to year. The assessments are usually in walking order of the parish, This is not necessarily true if the property is split up and sold or split between heirs, or if the land tax assessor has decided from a certain year to start arranging the list alphabetically. This sequence was gradually disturbed as separate lists were kept of owners who had made a one-off payment to redeem their Land Tax.

Reproduced by permission of the author, from work intended for use in the Birmingham Archive and Heritage Service. Part two can be read here.

{kind=link}

Comments

Add a comment about this page